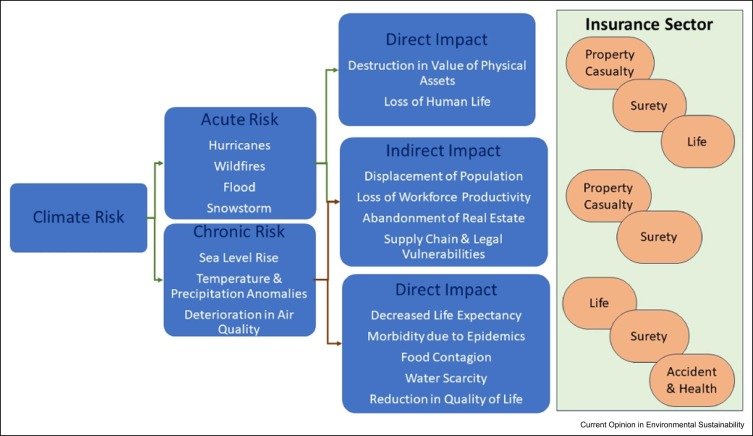

Impact of Climate Change on Insurance: Climate change is no longer a distant threat—it is a present-day reality affecting individuals, communities, and industries globally. In India, the insurance sector is facing increased pressure due to a rise in extreme weather events such as Cyclone Amphan, the devastating floods in Assam and Kerala, and the intense heatwaves across North India. These events have not only disrupted lives but have also strained the insurance industry by driving up the number and value of claims, particularly in the motor insurance and crop insurance segments.

The rise in climate-related claims has forced insurance companies to re-evaluate their risk assessment models. Previously, risk assessments were primarily based on historical data, but now insurers must account for erratic weather patterns and the unpredictability of climate events. Property damage, loss of crops, business interruption, and vehicle damage are among the top reasons why claims have surged. As a result, premiums have increased, and underwriting processes have become stricter. The need for climate resilience and adaptation strategies has become more urgent than ever.

In metropolitan cities like Bengaluru, for instance, unexpected rainfall has led to urban flooding, halting traffic and damaging vehicles en masse. A recent incident in May 2025 saw city buses and private vehicles stranded at Silk Board Junction due to waterlogging. Events like these serve as reminders of how quickly infrastructure can be overwhelmed, translating directly into high volumes of insurance claims. Consequently, insurance providers are compelled to redesign their coverage models and pricing strategies to address these evolving challenges.

Who Can Apply for Climate-Linked Insurance Policies?

Climate-linked insurance policies are primarily designed for individuals and entities most vulnerable to environmental damage. Here’s who can apply:

- Farmers and agricultural workers (for crop and weather-based insurance)

- Vehicle owners (motor insurance against flood or storm damage)

- Homeowners and property investors (property insurance against natural calamities)

- Businesses (commercial insurance for business continuity and damages)

- Urban dwellers in flood-prone areas

- Renewable energy firms (for protection against extreme climate events)

These groups are eligible to apply for various insurance schemes tailored to mitigate risks posed by unpredictable climate events.

Insurance Premiums and Fees: What to Expect

Insurance premiums in the climate context are highly dynamic and depend on several factors:

- Geographical location (e.g., coastal, flood-prone, or drought-prone areas)

- Type of insurance (motor, crop, health, property, or commercial)

- Frequency of past claims in the area

- Climate vulnerability index

- Sum assured and policy coverage terms

Typical crop insurance premiums under the Pradhan Mantri Fasal Bima Yojana (PMFBY), for example, range between 1.5% to 5% of the sum insured, while motor insurance premiums can vary depending on the add-ons for flood or cyclone protection.

How to Use Climate-Linked Insurance Wisely

Using insurance effectively involves more than just purchasing a policy. Here are some important tips:

- Choose the right type of coverage: Ensure your policy covers risks specific to your region (e.g., floods in Kerala or heatwaves in Rajasthan).

- Update your policies annually: Risks change, and so should your coverage.

- Keep digital copies of all documents: This is helpful during emergencies when physical copies are lost.

- Use add-ons: Many insurers offer optional riders such as engine protection, business interruption cover, etc.

- File claims promptly with photographic and video evidence.

Also read: Best Commercial Property Insurance in 2025: Top Providers, Fees, Benefits & How to Apply

Benefits of Climate-Smart Insurance

- Financial security during natural disasters

- Faster recovery after climate-related losses

- Access to credit for insured farmers and businesses

- Encourages better risk management practices

- Supports climate adaptation by incentivizing resilient infrastructure and farming

How to Apply for Climate Insurance Policies

Applying for climate-related insurance policies in India is now easier thanks to both offline and online options. Here’s a step-by-step guide:

Online Method:

- Visit the official website of your preferred insurance provider.

- Select the relevant policy (motor, crop, property, etc.).

- Fill in personal and risk-related details.

- Upload necessary documents (Aadhaar, land records, vehicle registration, etc.).

- Pay the premium.

- Receive the e-policy instantly.

Offline Method:

- Visit the nearest insurance office (LIC, Bajaj Allianz, HDFC Ergo, etc.).

- Talk to an agent and choose the right policy.

- Submit documents and pay the premium.

- Receive printed policy documents. Pradhan Mantri Fasal Bima Yojana (PMFBY)

Important Dates to Remember

| Event | Date |

|---|---|

| Monsoon Insurance Deadline (PMFBY Kharif) | 31st July 2025 |

| Crop Damage Assessment Window | August–October 2025 |

| Motor Insurance Renewal Window | Ongoing (depends on purchase date) |

| Flood Coverage Renewal Season | Pre-monsoon (March–May 2025) |

| Government Subsidy Declaration (PMFBY) | April 2025 |

Disclaimer

This article is for informational purposes only. While every effort has been made to provide accurate information, insurance policies and guidelines are subject to change. Always consult with a certified insurance advisor or check the official insurance websites for the most current details. Neither the author nor the platform is responsible for any decisions made based on this content.

Impact of Climate Change on Insurance Conclusion

Climate change is reshaping the global and Indian insurance landscape at an unprecedented pace. The frequency and severity of extreme weather events are pushing insurers to innovate rapidly while policyholders are now forced to think ahead and plan for contingencies that were once rare. The days of standard policies are behind us—customization, digital access, and quick response mechanisms are the need of the hour.

Insurance today is not just a financial product—it is a climate resilience tool. Whether you’re a farmer guarding your harvest, a homeowner in a flood zone, or a commuter in a busy city, understanding the new realities of climate-related risks can mean the difference between quick recovery and prolonged hardship.

As awareness grows, government schemes and private insurers are collaborating to provide timely protection and relief. However, much still needs to be done to ensure these benefits reach vulnerable populations in remote areas who often bear the brunt of climate disasters.

In conclusion, adapting to climate change with proactive insurance strategies is not a choice—it is a necessity. Stay informed, assess your risks, and secure your future with the right climate-conscious insurance policies.

Impact of Climate Change on Insurance FAQs

1. How is climate change increasing insurance claims in India?

Climate change is causing more frequent and severe weather events like floods, cyclones, and heatwaves, leading to massive damage to crops, vehicles, homes, and infrastructure. This results in a surge of insurance claims, particularly in the motor and crop insurance sectors.

2. Can farmers get financial support for crop loss due to climate change?

Yes, under schemes like the Pradhan Mantri Fasal Bima Yojana (PMFBY), farmers are compensated for losses due to floods, droughts, or other climate-related events. The government also subsidizes premiums to make the coverage affordable.

3. What types of insurance policies are most affected by climate risks?

The most impacted insurance segments include crop insurance, motor insurance, property insurance, and health insurance. These policies now need to cover a broader range of climate-related scenarios, increasing their complexity and cost.

4. Do insurance companies offer any incentives for climate-resilient behavior?

Yes, some insurers now offer discounts or lower premiums for climate-resilient infrastructure, green buildings, or safer vehicle parking zones. Others offer add-ons for proactive risk mitigation efforts like flood-proofing or sustainable farming practices.

5. What should one check before buying a climate-related insurance policy?

Before purchasing, ensure:

- The coverage includes natural disasters

- Premiums and exclusions are clearly mentioned

- Claim settlement history of the insurer is good

- The policy duration covers your risk window

- Add-ons are relevant to your geographical and climatic conditions